Forbes recently ran a contribution declaring Singapore to have a housing and credit bubble. Mr. Colombo will undoubtedly predict the next bubble and pop, since he has pointed to ten possible bubbles in the last three months. The amount of data he pulls together is very impressive. If you want an update on Singapore economic data I highly recommend the article.

He has tons of attention grabbing numbers, but the argument boils down to – low interest rates causing a credit bubble and correspondingly a housing bubble. He suggests that economic crashes in China and other parts of Asia (though he didn’t mention Thailand) plus rising interest rates will cause housing to crash, borrowers to default, and Singapore’s large financial industry to take everything down. After the collapse of US housing and the ensuing financial crisis, this all sounds reasonable.

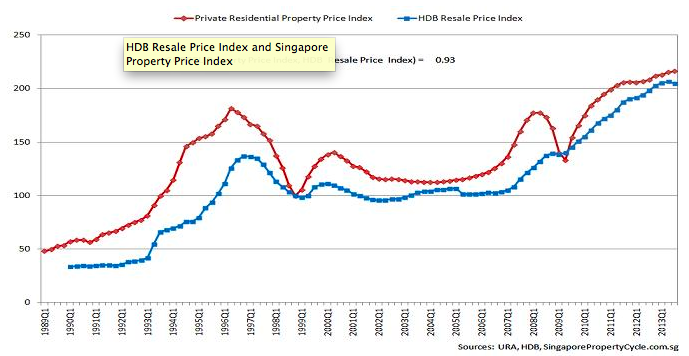

Except that Singapore’s housing and credit markets are different from the US. Starting with property, we see a volatile and recently bubble like trend:

Talking to property agents in 2010 and 2011, the market also sounded like a bubble – speculators were buying properties and reselling them very quickly, then reinvesting and driving prices. Singapore’s government did not follow Greenspan’s “I can’t see a bubble until it pops”. Instead, a number of “cooling measures” (economists would call these macro-prudential policies) were instigated to reduce speculation. These started as additional taxes for quick flipping of property. We can see in the next figure that the impact of the measures was significant. In fact, the initial reports for December 2013 indicate a drop in housing prices. Again, my agent contacts are all saying that volumes are way down. And I’m hearing anecdotes of housing selling below valuations (unheard of in the previous decade).

Now remember that these private properties are actually less than 20% of the market. We should be looking at public housing:

{kind=link}

Here we all see a big run up in prices from 2007 to today (with a down-blip at the end). But we can also see an eight-year stretch of no housing price increases. Overall we have 6% per year from 1999 to today, or 4% yearly appreciation, which doesn’t sound so much like a bubble. We should also check the supply and demand fundamentals:

{kind=link}

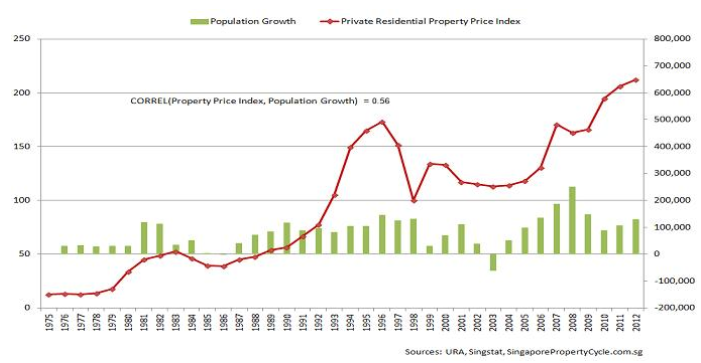

So construction of new units was low and flat in the 2000s and recently increased. Compare with population growth:

{kind=link}

The mid-2000s had a big influx of immigrants while housing supply was not growing to match. Unsurprisingly, prices increased rapidly.

The original claim was that the ‘bubble’ was caused by ultra-low interest rates leading to unsustainable borrowing. While interest rates clearly did lead to a lot of borrowing there are reasons to believe there will not be a crash in Singapore. My first reason for being optimistic is that the most recent ‘cooling measures’ have been macro-prudential regulations targeted at excessive borrowing. The Monetary Authority of Singapore announced in 2013 that a small percentage of Singaporeans were taking on dangerously high debt service levels. To curb this, various policies were enacted. In early 2013 a limitation on loan-to-value and debit levels on car loans. This instantly hammered the “private transport” inflation from 5% to zero. In mid 2013 the Monetary Authority of Singapore put new restrictions on property loans. These featured caps on loan to value (80% on first property; 60% on a second property) and total debt service ratio (60% for all loans against haircut income). Significantly the total debt service ratio must be calculated as if interest rates were 3.5% or higher – not at current low rates.

The caps on additional property and total debt service ratio are particularly meaningful in Singapore. While home-equity loans in the US were used to fund home extensions and cars, in Singapore they tend to be used to purchase additional property for rental income. This means that actual re-payment is less sensitive to employment than it was in the US. Further, employment is very high in Singapore.

Mr. Colombo raised concerns about an overheated construction sector as well. The first item to allay concerns is that the significant investment in infrastructure will continue for at least another decade. Two more pan-island subway lines are planned for start in the next decade as are several extensions to existing lines. Additionally, never underestimate Singaporeans desire to rebuild their apartments. Residential housing in Singapore rarely lasts even 20 years, and so the construction industry will be sustainable even just refreshing the existing housing stock.

Finally, even a large global recession may not have lasting impact on Singapore. The Singapore economy was hit significantly by the global financial crisis. However, the recovery was very quick – 1 or 2 years depending on how one counts. Singapore has two big safety nets for recessions. Most important, normally running a surplus, Singapore is able to engage in very significant short-term stimulus spending – on the order of 10% of GDP for 2009. Secondarily the extensive importing of labor provides a safety valve – foreign workers are laid off first, and so unemployment never gets very high. Additionally, Singapore’s export markets are quite diversified with Europe, China, Malaysia, Indonesia, Hong Kong each about 10% and US a little less than that. While an economic crisis in China would be bid news for Singapore, I don’t see that as likely to cause a credit crash in Singapore.

Not everything in Singapore is roses however. While I don’t a crisis in the near future, I do have concerns about medium-term growth trends. As shown in the graph above, population growth has been quite strong over the last ten years. This has strained housing availability (evidenced by the prices), transport infrastructure, and particularly the political climate since most of the population growth has been immigration. These strains have resulted in a number of restraints on immigration. In spite of a government goal to add another million people, population growth will slow for the next several years while infrastructure catches up. The slower importation of labor will also pressure wages, particularly in lower skill industries.

Conclusions:

While house prices have been high and interest rates low, I believe there is no imminent crash. While emerging markets have been hit hard, Singapore is not an emerging economy – it is a developed nation, with a strong economy, full employment, and enjoys a ‘safe haven’ status for regional wealth. While the big returns of the 80s and pre-crisis 90s are unlikely, returns to Singapore companies (EWS) and Singapore small caps (EWSS) are likely to be reliable. Both the EWS and EWSS funds give a sustainable 4% yield. Investors looking for a good entry point should pay close attention to the exchange rate (FXSG) and bargains due to spill over effects from capital outflows from emerging markets. The exchange rate history suggests a 2 to 2.5% annualized appreciation adding to the 4% dividend stream. Thus I feel Singapore is still an acceptable place for investment – risks are lower than the market is implying.

Disclosure: I am long EWS, EWSS. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

iShares MSCI Singapore Index Fund (ETF) (EWS) news: Singapore: Bubble ...

Không có nhận xét nào:

Đăng nhận xét