I was stepping off the plane when the idea for this article came to me. I was just returning home from several months living in the Haidian district of Beijing and I was attempting to process everything that I had seen. That trip revealed to me the disconnect between my expectations and the realities of modern China. This country is simultaneously both so much more developed and so much less developed than you can imagine. The infrastructure is modern and expansive and the entrepreneurial spirit is alive and well amongst its people. In contrast, however, laws are seen as guidelines, censorship is rampant, the population truly massive and there are still remnants of an impoverished society — I witnessed a traffic jam involving nothing more than people and bikes (to say nothing about the squat toilets, science notwithstanding).

It was an awesome opportunity to see a country on the move. Naturally, looking at such a country begs the question as to where it is moving. That potential future is what I will attempt to discuss in this article. To understand China’s future, I will first look at where it now stands, and then I will attempt to look at some possible scenarios relative to where it might be going. These scenarios cover a spectrum of possibilities and could be categorized as “Bullish,” “Neutral,” and “Bearish.” In each scenario, which would potentially play out over the medium to long term (i.e., five years or more), I will lay out the main forces at play, the issues and characteristics of each scenario, what the world in 2019 will look like, and finally, what impact the various scenarios will have on the markets.

Where We Are Now

We are faced with a shift in the international system caused by the rise of China. China has experienced more than 30 years of uninterrupted growth, resulting in its current position as the second largest economy in the world. China found a model that worked incredibly well – an investment driven export boom financed on the back of a huge population and easy credit for State Owned Enterprises (SOEs). That model, however, is breaking down. China is experiencing skyrocketing inequality, rising political dissent, and an unfolding environmental disaster.

Chinese leaders are very intelligent. They recognize these problems and are attempting to keep the party going with a new wave of economic reforms – the Third Plenum, and the potential signing of a Bilateral Investment Treaty (BIT) with the United States. In order to keep the party going, however, they must ditch the old model of investment driven growth and adopt a focus on sustainable consumption driven growth. There is, however, the fear of a so called “Gorbachev Moment,” when reforms unleash forces far beyond the architects’ ability to control. This is where things get interesting. Consumption driven growth is reliant on a burgeoning middle class which historically demands more politically as it gets wealthier. China’s Communist Party is going to have to thread the needle between the imperative of maintaining growth, and the imperative of staying in power.

Source: Yukon Huang via FT Alphaville.

The pressure for reform is occurring amidst China’s recent ascension to middle income status. While salutary, it comes with the threat of the so called “Middle Income Trap,” whereby economic growth slows precipitously as a country reaches an income level of between roughly $5,000 and $12,000 per capita. At this phase, the old catalysts for economic growth, such as: technology imports, massive urbanization, and cheap labor, start to run dry. In order to continue growing, a country must transition to competing at the technological frontier. This is not an easy transition to make, however, as it relies on world-class education systems, RD, and high value-added goods. China’s advantages in infrastructure and demographics have relatively less impact at the technological frontier. In the past, failure to adjust to this new reality has left numerous other middle-income countries by the wayside.

Reform is made more difficult by the Chinese government’s significant degree of factionalism. The government places a great deal of emphasis on presenting a unified face to the world, however, rifts within the political power bases are growing. While divides in opinion were always present, past Chinese leaders wielded significantly more authority and were better able to paper over the divides. As each generation steps down, they retain more and more influence, diluting the current leaders’ power. Jiang ZeMin, in power from 1993 to 2002, was seen as the “winner” of the recent leadership transition by having five allies — as opposed to Hu JinTao’s one ally — placed on the Politburo, according to The Diplomat. While these factions are not necessarily ideologically driven, they all have specific interests in shaping reforms — such as SOEs. Any reforms must appeal to the self interests of the various factions in order to be effectively executed.

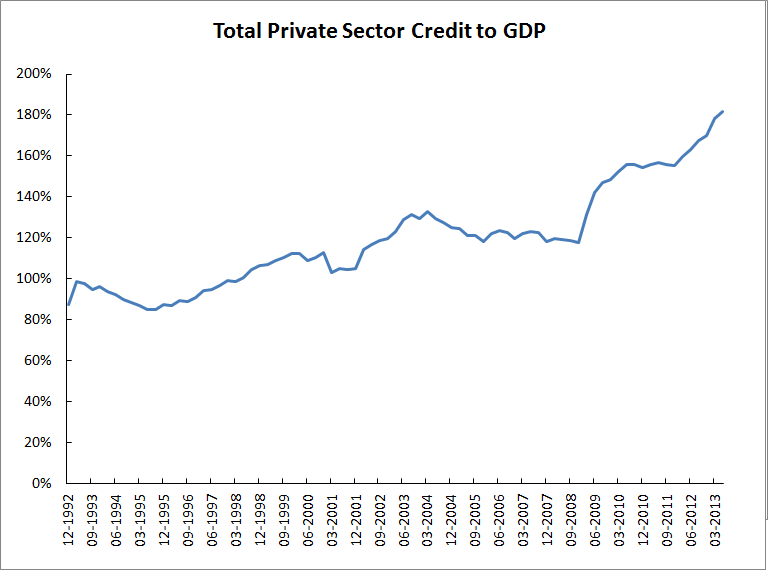

In the near term, China’s leaders will have to deal with two potential threats looming in the credit market and the real estate market. The size of a potential credit bubble is likely to be the bigger of the two immediate threats, caused by a lack of trust in equity markets and in other relatively stable sources of financing common in the West. This bubble has been in existence for decades, however, China’s rapid economic growth enabled it to literally grow out of the potential problem. With economic growth slowing down, as China embraces consumerism, it is possible that the credit levels may be unsustainable.

Click to enlarge images.

{kind=link}

Source: Peterson Institute for International Economics.

However, this may not be the case if China plays its card right. Chinese regulators seem to be well aware of the potential problem and have been focused on deflating it — as seen from the miniature credit crunch this summer. Likewise, China has experienced a massive rise in real estate prices all over the country. News reports such as “China’s Crazy Property Bubble” harp on massive housing complexes going up all over China with no one living in them. There are two relevant points here. First of all, China has a great deal of capital controls that limit access to solid investments. This increases the incentive for the rich to place their new found wealth into housing, an incentive that could easily be changed with reforms. Secondly, one must remember that as a consequence of China’s extremely high savings rate, the vast majority of houses are purchased with cash, not mortgages or other deft-financing vehicles. This limits the risk of there being uncontrollable contagion leaking out of a malinvested real estate bubble, like the one that tipped the U.S. into recession in 2008.

Ultimately, with the appropriate response, both of these threats can be dealt with. What happens next is of massive importance to the world. Therefore, it is important to study these potential events and to try to understand their myriad effects on the future. When attempting to look into the future, it is impossible to know with certainty what will happen. Rather, an approach that attempts to map a range of future possibilities is more likely to get at least a couple of correct predictions.

Future Scenarios

1. The Bullish Scenario

The Bullish Scenario fundamentally revolves around China carrying out economic reforms while simultaneously managing to gradually open up politically. Problems with housing and credit are successfully dealt with, at the same time that wide ranging economic reforms are enacted. These reforms must deal with three main issues. First, China must support workers who serve as the primary basis for consumption. Secondly, China must make financial reforms and reform SOEs in order to better support private businesses. Finally, small scale experiments in decentralized governance should be continued. As well as the above, a positive impact may result from the United States and China successfully signing and implementing the BIT, thus removing market barriers and increasing competition.

Needed reforms involve changes to China’s labor market. China’s wages have not kept track with the marginal product of labor, depressing workers’ share of China’s economic gains and causing a fall in consumption. This was seen with household income rising over the last three decades, but experiencing a simultaneous decline in its share of GDP from over 60% in the 1980s to just 41% recently. China could take a number of steps to reverse this trend. According to Linda Yueh in “China’s Strategy towards the Financial Crisis and Economic Reform,” these steps could include reforming the Hukou System. The Hukou is a registration and identification system wherein residents are classified as belonging to a certain place, and can only receive benefits in that place. Reforming this system would enable migrant residents of cities to gain access to social services, limiting the need to save and thus increasing consumption. This would also increase the mobility of the labor market and provide more opportunities for workers. Likewise, such reforms would improve the effectiveness of China’s ongoing urbanization by providing both economies of scale in service delivery, and new opportunities for business.

{kind=link}

Source: Tom Orlik on WSJ.

Financial system reforms are also necessary to fundamentally solve these problems. These could take the form of boosting the reliability of equity markets (via increased regulation and oversight), continuing the liberation of interest rates, easing capital controls, and allowing private banks to do more. Banking in China is currently mostly in the hands of the state, and dominated by four large state owned banks. These banks give most of their attractive loans to SOEs. This has led to a credit crunch for private companies in China, and has caused Chinese firms to save an excessive amount. Without access to the easy credit that SOEs have, or trustworthy equity markets, private firms often rely on retained earnings in order to grow. With the necessary reforms, China could bring stability to its financial system, and limit the risk of the so called “hard landing”. These reforms would provide new sources of capital for private firms that make more efficient usage of resources, thus boosting economic growth in the long run.

The degree to which China manages to reform its State Owned Enterprises (SOEs) could also have an impact on whether the Bullish Scenario occurs. Far from being the much heralded model of state directed capitalism, SOEs have proven to strangle the stock market, limit financing to innovative private firms (the majority of banks are state owned and only loan to state companies), and generally misdirect investment. All of these effects have resulted in a less liquid and effective financial system, and less profitable economy. China’s leaders have stated that they will attempt to limit the systemic bias towards SOEs, while reforming SOEs incentives. This could make the Chinese SOEs look more like Singapore’s Government Linked Companies (GLCs), which are managed by a large sovereign wealth fund — Temasek — where the focus is on increasing returns, not serving political purposes.

Governance reforms are another crucial aspect to the occurrence of the Bullish Scenario. In the medium term, these reforms are likely to take three main forms: improving governance at the local level, supporting civil society and establishing a strong and independent judiciary. These three reforms are important, albeit for different reasons. Improving governance at the local level such as providing limited democracy could serve as a model for the rest of the country later on. Indeed China has shown a preference for such bottom up transformations in the past (i.e., China’s transition to capitalism). China could also move towards enabling an actual civil society with NGOs providing valuable services. This contrasts with China’s current “GONGO” system (government organized non government organizations). Similarly, a strong and independent judiciary would limit corruption, and boost transparency while simultaneously making investing clearer and easier. This could take the shape of separation of the administrative, and judicial branches of the government.

Evidence of the viability of the Bullish Scenario can be found in the potential signing of the Sino-U.S. BIT. While much remains to be done, since the breakthrough in July, interests are more aligned on the topic than ever. This will have a number of important effects for both Chinese, and American firms. It will open up a number of sectors to competition from U.S. firms, increasing economic efficiency. This would also increase the capacity for companies to invest in each other, providing significant new avenues for growth.

If China successfully enacts these reforms and avoids a credit or housing bust, China in 2019 would be a far wealthier place. It would have surpassed the United States to become the World’s richest country. With the noted reforms, China could build on progress made to date. It would have a number of burgeoning private sector champions (Xiaomi, Alibaba, Huawei) that already have been gaining increasing market share in both developing, and developed markets. While a number of high value-added industries (aerospace, consumer technology) would remain dominated by the United States and Europe, China would increasingly become a hotbed of innovation. This would be balanced out by a resurgence of developed country manufacturing, as China’s domestic market would finally reach its consumption potential.

Similarly, under the Bullish Scenario, in five more years, China’s political system would be much more flexible. The makings of a strong, legal infrastructure would be starting to appear as the judiciary gained increasing confidence and independence. While censorship may continue, village democracy would be more widespread as China attempted to fight corruption, and promote organic growth. China would be well on the road to becoming a superpower.

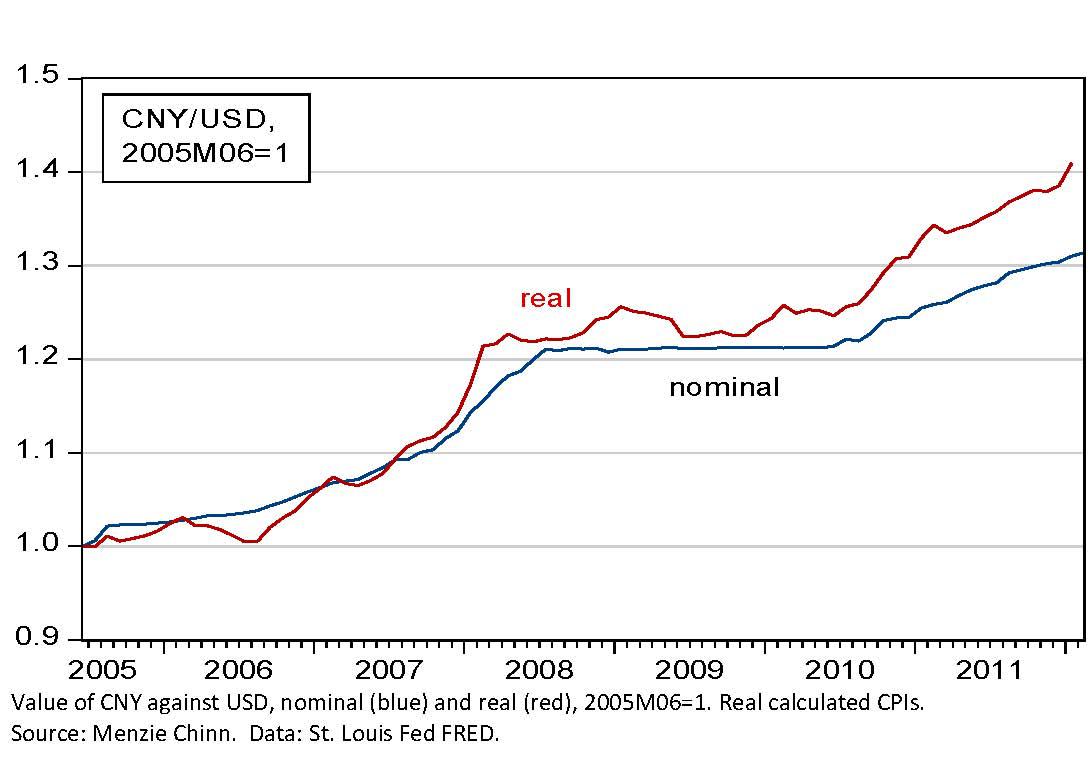

In the world of the Bullish Scenario, there are a number of market opportunities for the shrewd investor, many of which would be based on the resurgence of U.S. exports. China’s switch to a consumption driven model will make its people both more willing, and more capable of purchasing imported goods. Also, the limiting of capital controls and For-Ex regulations, allowing the currency to float freely, should boost the Yuan’s value, especially given its rising importance in the global economy. These trends are already reflected in China’s rapidly appreciating currency versus the U.S. dollar. This should make U.S. goods relatively more competitive, and result in a boost to U.S. exports. Therefore, struggling U.S. manufactures (or thriving ones) should gain a second wind from the Bullish Scenario. Investors looking for exposure to these trends should look at ETFs such as Industrial Select Sector SPDR (XLI) or large U.S. industrial players such as General Electric (GE).

{kind=link}

Source: Jeff Frankels Weblog on China — “China Adjusts.”

China’s equities will also prove to be a good investment in the Bullish Scenario. Over the last two decades, China has had one of the worst performing markets in the world. Its financial markets are dominated by SOEs that allocate capital based upon the whims of the state, and not just what is profitable. Accordingly, their performance has been terrible. Under the Bullish Scenario, ETFs such as iShares China Large-Cap ETF (FXI), and private firms such as Baidu (BIDU) or Youku (YOKU) could experience significant appreciation. SOEs should not do as well, and should consequently be avoided.

2. The Neutral Scenario

The issues and results stemming from the Neutral Scenario are much less clear cut than the Bullish Scenario. In this scenario, China’s reforms are a mixed bag of achievements. Some things are carried out effectively, however, really heavy hitting reforms never occur. At the same time, nothing spectacular goes wrong and China manages to hold off a financial crisis. China merely muddles through the next five years, with steadily slowing growth rates.

The main catalyst for the existence of the Neutral Scenario is a failure to reform the SOEs. Reforming SOEs is in many ways more of a political issue than an economic one. They are massively powerful with a huge number of employees (many of which are communist party members who are relatively more influential in Chinese society). In a factional system such as China’s, the pressure to limit SOE reform is great. In this context, China may attempt to boost the competitiveness of private firms, while leaving the SOE structure largely in place. In fact, this already seems to be happening, with SOEs previous decline in market share stabilizing over the last couple of years.

Source: World Bank 2030 Report, p. 111, via Tom Conley.

In the Neutral Scenario, China in 2019 will look very similar to how it looks now. Growth, however, will be slowing since marginal reforms would fail to create a new engine for economic growth. Politically, reforms would be limited and China’s government would be resorting to increasingly nationalist propaganda in order to stem criticism. Ultimately, 2019 would be a year of choices in China. The need for structural reforms would still be present, however, procrastination would mean that the costs would now be higher. What China’s leaders do next would have a big impact on whether or not it escapes the “Middle Income” trap.

In the event of the Neutral Scenario occurring, SOEs such as China Mobile (CHL) should perform well over the medium term. FXI should perform moderately well, with decent gains. However, those looking for rapid gains might want to look elsewhere considering the overall level of risk. U.S. stocks should perform well since ongoing catalysts such as shale gas, efficient capital markets, excellent universities, and a large consumer-driven market would continue to boost the U.S. economy. In this scenario, China’s performance will have relatively less impact on U.S. markets, as compared to U.S. domestic policy. General ETFs such as iShares SP 500 Index Fund (IVV) should do well in conjunction with the U.S. economy.

3. The Bearish Scenario

The Bearish Scenario is where things get interesting. In many ways, it could be seen as the polar opposite of the Bullish Scenario. Just as the Bullish Scenario eventually relies on China’s leaders ability to effectively rein in SOEs, reform its labor and financial markets, and gradually open up politically, the Bearish Scenario envisions that none of those reforms are either put in place or are successful.

As previously stated, China’s politics are characterized by a number of competing factions. Roughly speaking, there are reformers, pragmatists, and hardliners. Reformers currently have the upper hand, thanks to the support of the pragmatists. The pragmatists recognize that without opening up economically, the Communist Party is doomed. The hardliners, however, draw their base of support from SOEs and other institutions that could be losers if structural reforms are put in place. In the event of a “Gorbachev Moment” (or the appearance of the possibility of one), the hardliners could come back to the fore and double down on the old model. Indeed, after the Tiananmen Square protests, economic reforms were halted. It was only after Deng Xiaoping (a figure far more powerful in China than anyone comparable today) began his southern tour that they got going again. To say the least, this halting of reforms would be a disaster. Growth would fall to lower and lower levels, as the marginal productivity of China’s investments would fall off a cliff.

As it stands now, China has seen its debt-to-gdp ratio explode to 207% of GDP in the last six years. Considering the poor regulation of banks, this credit expansion involved a number of bad loans that were pushed off the balance sheet, thus hiding the true extent of China’s debt problems. Estimates routinely place these bad loans at 10% of GDP, and sometimes as high as 25%-30% of GDP. This is enabled by China’s banks being largely state owned and thus prone to allocating capital based upon the whims of government bodies (bodies who historically haven’t been very effective economically). While these investments usually pay a social dividend, such as by boosting employment, they often fail to generate adequate financial returns. Furthermore, banks are the dominant source of lending due to the undeveloped nature of Chinese capital markets (again, something that would not change in the Bearish Scenario). These banks loan cheaply to SOEs, however, charge private firms interest rates as high as 20%. This pushes private firms into proliferating wealth management vehicles that are poorly regulated and understood, or real estate, possibly enabling the burst of a credit or housing bubble.

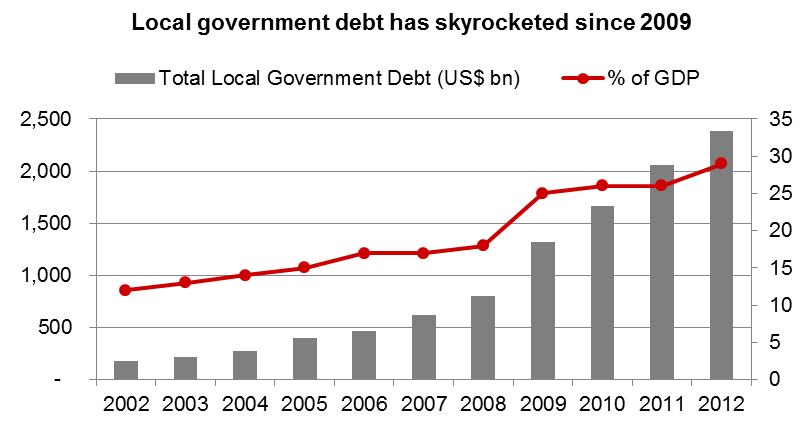

Furthermore, China’s local governments have an increasing amount of debt that they finance by expropriating land and either selling it to real estate developers, or developing the land itself. This is a cycle whereby debt levels are increased, and then financed by increasing leverage to the housing market. Although all land is nominally owned by the state, many people who lose their home don’t view it that way. This is a growing source of tension in China as evidenced by the rapidly growing number of “mass incidents”. Similarly, the marginal returns of these investments are falling as evidenced by the rising amount of credit as a share of the economy. Overall, this system works very well until it doesn’t (see 2008 in the United States).

{kind=link}

Source: Frontier Strategy Group.

As China attempts to head off a booming housing market, and a potential credit bubble, regulators could exacerbate these problems by tightening credit conditions and raising interest rates without economic reforms. The combination of these events could result in a credit crunch and hard landing that make the great recession look like a walk in the park.

Under the Bearish Scenario, China in 2019 would be a country on the verge. Environmental degradation and failure to undertake land reform would have exacerbated rural and urban tensions, leading to a skyrocketing number of mass incidents. In order to cope with this, China’s leadership would be acting increasingly aggressive abroad as they attempt to shore up support at home. This would likely lead to rising trade tensions that would result in a growing headwind due to China’s ongoing reliance on global trade. The makings of this are already in play with a tariff row over solar panels, the recent rare earth export ban to Japan, and competing trade blocs developing in the Pacific (China’s RCEP vs. the U.S. TPP). Meanwhile, the Chinese economy would be in the midst of a massive correction after a failure to adjust away from a three-decade long credit-fueled export boom.

The important question under the Bearish Scenario is how will these developments would affect the financial markets? One of the most obvious impacts would likely be on China focused ETFs, such as FXI. If a Bearish Scenario starts developing, sell and sell fast. Growth will slow precipitously, and China could experience a correction of historic proportions that erases profits and shareholder value. Gold and inverse ETFs, such as ProShares UltraShort FTSE/Xinhua China 25 (FXP), would prosper in this Scenario.

Another way to hedge bets would be to shift funds back to the United States. While the U.S. economy would likely be hammered by a Chinese hard landing, the U.S. economy has proved itself to be one of the most resilient in the world, and is likely the safest place for long-term shareholder return. General large-cap focused ETFs could serve as a good defense against the Bearish Scenario.

Conclusion

Ultimately, I am relatively bullish on China. I think the most likely future scenario by far is some combination of Bullish-Neutral. Over the last 30 years, China’s leaders have demonstrated some of the most effective governance in human history. That governance is now being put to a test. However, I am of the opinion that China will pass this test and continue growing (albeit at a much more moderate pace). They have a massive and entrepreneurial population that should prove to be a significant catalyst going forward.

Whatever happens, investors looking at China must make sure to do their own due diligence. If you are interested in investing in China, look at the degree to which China’s leaders reform SOEs. As I discussed within this article, the status of SOEs is perhaps the most crucial issue determining China’s long-term economic success. Also, in the near term, watch out for the Fed Taper since the end of Quantitative Easing is usually associated with funds flowing away from riskier emerging markets towards more stable investments.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Looking Into The Crystal Ball: Scenarios For China"s Future

Không có nhận xét nào:

Đăng nhận xét