For U.S.-based investors, there are many sources to get access to information regarding FedEx Corporation (FDX) and the United Parcel Service, Inc. (UPS). While most investors probably are familiar in some form with Deutsche Post DHL’s (DPSTF.PK)) competitive services, getting comprehensive information for the company is not so easy based on the simple fact that it trades on the German stock exchange and is not publicly listed in the U.S.

Understanding DHL’s comparative business segments and operations as they relate to both FedEx and UPS is a crucial piece to the analysis framework when considering investments in either U.S. company. For this reason the article will provide an overall assessment comparing all three companies and the analysis will be structured into the following areas:

- Industry Overview

- Business segments

- Revenues and competition

- Key growth drivers

- Fundamental peer review

INDUSTRY OVERVIEW

It is important for investors to consider some high-level factors which directly impact FedEx, UPS, and DHL. Two primary variables that always play a role in the demand for package delivery, freight, and supply chain are the growth of the global economy and secondarily, the price fluctuations of oil.

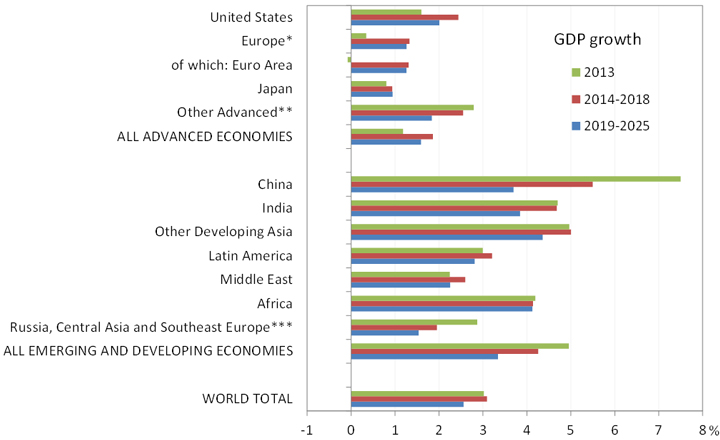

Global Outlook for Growth of Gross Domestic Product, 2013-2025 (May 2013)

(Click to enlarge)

Europe includes all 27 current members of the European Union, as well as Iceland, Norway, and Switzerland.

**Other advanced includes Canada, Israel, Korea, Australia, Taiwan, Hong Kong, Singapore, and New Zealand.

***Southeast Europe includes Albania, Bosnia Herzegovina, Croatia, Macedonia, Serbia Montenegro, and Turkey.

Source: The Conference Board Global Economic Outlook 2013, May 2013 update

Global Outlook for Growth of Gross Domestic Product, 1996-2013 (May 2013)

1996 – 2005

2006 – 2012

2012

2013

Distribution of World Output 2012

GDP Growth

Contribution to World GDP growth****

Projected GDP Growth

Contribution to World GDP growth****

Projected GDP Growth

Contribution to World GDP growth****

Projected GDP Growth

Contribution to World GDP growth****

United States

18.2%

3.3

0.7

1.1

0.2

2.2

0.4

1.6

0.3

Europe*

20.3%

2.4

0.6

0.9

0.2

-0.2

0.0

0.3

0.1

of which:

Euro Area

13.8%

2.2

-

0.7

-

-0.5

-

0.1

-

Japan

5.6%

1.0

0.1

0.2

0.0

0.6

0.0

0.8

0.0

Other advanced**

7.2%

4.0

0.3

3.0

0.2

2.2

0.2

2.8

0.2

Advanced Economies

51.3%

2.7

1.7

1.2

0.7

1.1

0.6

1.2

0.6

China

16.4%

8.1

0.6

10.4

1.3

7.8

1.2

7.5

1.2

India

6.3%

6.5

0.3

7.8

0.4

5.5

0.3

4.7

0.3

Other developing Asia

5.3%

3.9

0.2

5.0

0.2

5.3

0.3

5.0

0.3

Latin America

7.7%

2.8

0.2

3.7

0.3

3.1

0.2

3.0

0.2

Middle East

3.7%

4.6

0.1

4.3

0.2

5.5

0.2

2.2

0.1

Africa

3.3%

4.6

0.1

4.7

0.1

3.7

0.1

4.2

0.1

Russia, Central Asia and Southeast Europe***

5.9%

4.0

0.2

4.0

0.2

3.6

0.2

2.9

0.2

Emerging and Developing Economies

48.7%

5.0

1.8

6.5

2.8

5.5

2.6

5.0

2.4

World Total

100.0%

3.6

3.5

3.2

3.0

*Europe includes all 27 current members of the European Union, as well as Iceland, Norway, and Switzerland.

**Other advanced includes Canada, Israel, Korea, Australia, Taiwan, Hong Kong, Singapore, and New Zealand.

***Southeast Europe includes Albania, Bosnia Herzegovina, Croatia, Macedonia, and Serbia Montenegro, and Turkey..

****The percentage of contributions to global growth are computed as log differences and therefore do not exactly add up to the percentage growth rate for the world economy.

Source: The Conference Board Global Economic Outlook, May 2013 update.

The above information, courtesy of The Conference Board, displays historical trends of global GDP growth as well as forecasts for short-term and mid-term time horizons. Most interesting to note is that post 2005 trends, advanced economies have witnessed a decline in GDP growth trends of over 50%, while emerging and developing economies have remained stable. For the mid-term horizon year, world total GDP growth is expected to continue its overall downward trend.

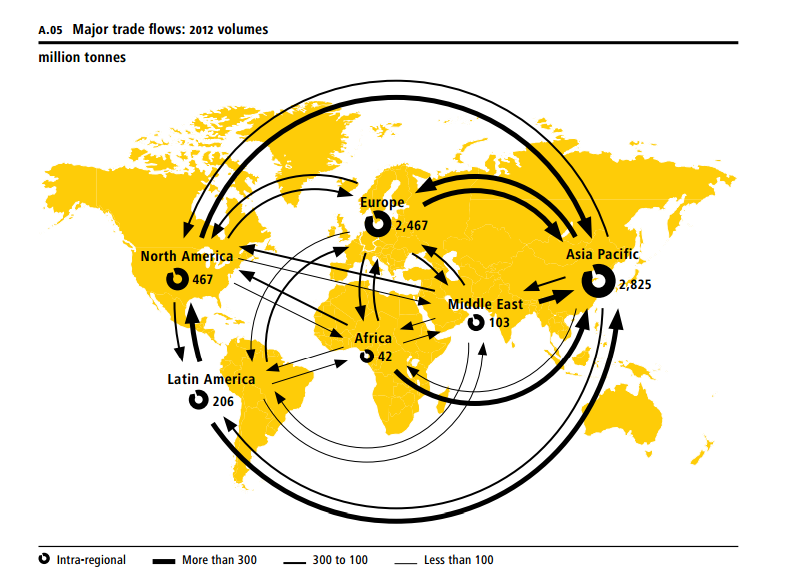

The diagram below depicts major global trade flows between regions. Based on world GDP growth of 3%, this diagram provides a snapshot of 2012 trade volumes. A key observation is the significance of the Asia Pacific region (China most notably) as the largest regional importer in the world with more than 300 million tons of trade flows coming from each North America, Latin America, Europe, Africa, and the Middle East.

(Click to enlarge)

Source: DHL Annual Report 2012

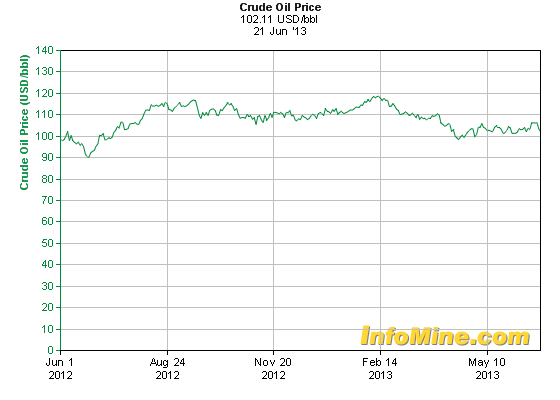

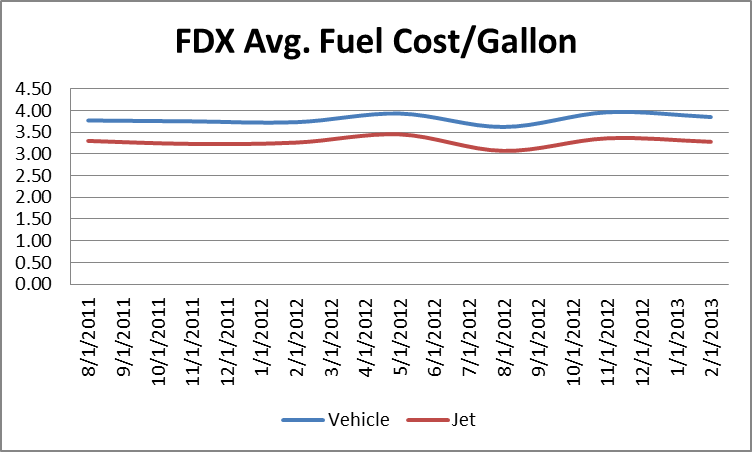

Over the past year oil prices have fluctuated significantly between $90 per barrel and $120 per barrel. To date prices for oil have declined from the February 2013 peak near the year’s low. FedEx’s recent May year-end earnings report mirrors this decline as their overall fuel costs decreased year-over-year between 2012 and 2013.

(Click to enlarge)

(Click to enlarge)

BUSINESS SEGMENTS

FedEx operates the following business segments, FedEx Express, FedEx Ground, FedEx Freight, and FedEx Services. For an overview of FedEx’s business or information please refer to their most recent 10-K filing.

FedEx Express is the pioneer for express distribution and claims to be the industry leader in this segment. FedEx Express offers domestic overnight and deferred package and freight services, as well as international express and deferred package and freight services.

The company also provides domestic air transportation services to the United States Postal Services, or USPS, for First-Class, Priority, and Express Mail, a contract was renewed earlier this year.

FedEx Express’s primary sorting facility, located in Memphis, serves as the center of the company’s multiple hub-and-spoke system. A second national hub facility is located in Indianapolis. In addition to these national hubs, FedEx Express operates regional hubs in Newark, Oakland, Fort Worth and Greensboro and major metropolitan sorting facilities in Los Angeles and Chicago. Facilities in Anchorage, Paris, Guangzhou and Cologne/Bonn serve as sorting facilities for express package and freight traffic moving to and from Asia, Europe and North America.

Through FedEx Trade Networks the company also provides international trade services, specializing in customs brokerage and global ocean and air freight forwarding. FedEx Supply Chain Systems provides a range of supply chain solutions utilizing FedEx information technology and transportation networks around the world.

FedEx Ground is a leading provider of business and residential ground package delivery services. FedEx Ground serves customers in the North American small-package market, focusing on business and residential delivery of packages weighing up to 150 pounds.

FedEx Ground operates a multiple hub-and-spoke sorting and distribution system consisting of 525 facilities, including 33 hubs, in the U.S. and Canada. FedEx Ground conducts its operations primarily with 30,770 owner-operated vehicles and approximately 35,000 company-owned trailers.

As FedEx Ground relies on independent contractors for its owner-operator operations, investors should take note regarding the fact that the company is involved in numerous lawsuits and other proceedings (state tax audits or administrative challenges) where the classification of its independent contractors is at issue. Item 1A of the Annual Report Form 10-K above and Note 17 provide more information.

FedEx SmartPost (a subsidiary of FedEx Ground) is a leading national small-parcel consolidator, which specializes in the consolidation and delivery of high volumes of low-weight, less time-sensitive business-to-consumer packages, using the USPS for final delivery to residences. The company picks up shipments from customers (including e-tailers and catalog companies), provides sorting and linehaul services and then delivers the packages to a USPS facility for final delivery by a postal carrier.

FedEx Freight is a leading North American provider of less than truckload, or LTL, freight services including FedEx Freight Priority and Economy. FedEx Freight serves every U.S. ZIP code, Canada, Mexico, Puerto Rico, and the U.S. Virgin Islands. As of May 31, 2012, FedEx Freight was operating approximately 58,000 vehicles and trailers from a network of 366 service centers.

FedEx Custom Critical provides a range of expedited, time-specific freight-shipping services throughout the U.S., Canada, and Mexico. Freight brokerage solutions are included.

FedEx Services provides the other FedEx companies with sales, marketing, information technology, communications, customer service, and certain other back-office support.

FedEx Office provides a network of digitally-connected locations and offers access to copying and digital printing through retail and web-based platforms, signs, and graphics, professional finishing, computer rentals, and the full range of FedEx day-definite ground shipping and time-definite global express shipping services. This segment has been bolstered primarily by the acquisition of Kinko’s roughly 9 years ago.

UPS operates the following business segments, U.S. Domestic Package and International Package under the Global Small Package area; and Supply Chain and Freight. For an overview of UPS’s business or information please refer to their most recent 10-K filing.

Within the U.S. Domestic Package segment, UPS is a leader in time-definite, money-back guaranteed, small package delivery services; offering ground and air package transportation. Options include same/next day, deferred, ground, or UPS SurePost for non-urgent, light weight residential shipments. UPS SurePost, similar as FedEx’s SmartPost utilizes the USPS for final delivery.

International Package includes small package operations in Europe, Asia, Canada, and Latin America. Services include time-definite express options as well as palletized freight shipment needs; non-urgent deferred services are available including cross-border ground package delivery which is offered within Europe and between the U.S. and Canada and the U.S. and Mexico.

Europe is UPS’s largest region outside of the U.S. and accounts for roughly half of international revenue.

UPS was not successful in its attempt to acquire TNT Express, which would have significantly expanded its European presence. TNT Express is the fourth largest package delivery and logistics company (€7.2 billion 2012 revenue) behind FedEx, UPS, and DHL.

UPS considers growth opportunities in Germany, the United Kingdom, or U.K., France, Italy, Spain, and the Netherlands and as a result is expanding their main European air hub in Cologne, Germany by 70% to a capacity of 190,000 packages per hour.

UPS is also focusing on growing operations in intra-Asia trade including China. UPS serves more than 40 Asia-Pacific countries and territories through more than two dozen alliances with local delivery companies that supplement company-owned operations.

The Supply Chain and Freight segment consists of forwarding and logistics services, the UPS Freight business, and financial offerings through UPS Capital.

UPS is one of the largest U.S. domestic air freight carriers and among the top international air freight forwarders globally. Additionally, as one of the world’s leading non-vessel operating common carriers, UPS also provides ocean freight full-container load and less-than container load shipments between most major ports around the world. UPS is also among the world’s largest customs brokers by both the number of shipments processed annually and by the number of dedicated brokerage employees worldwide.

Logistics and distribution includes distribution centers for storage and shipment, customer stock support, and other mail services. UPS Freight offers regional, inter-regional, and long-haul LTL services as well as full truckload services in the U.S., Canada, Puerto Rico, Guam, the U.S. Virgin Islands, and Mexico. UPS Capital offers a range of services, including export and import financing to help improve cash flow, risk mitigation, etc.

DHL operates the following business segments; Mail, Express, Global Forwarding, Freight, and Supply Chain. For an overview of DHL’s business or information please refer to their most recent annual report.

DHL is the only provider of universal postal services in Germany. In the Mail segment, DHL delivers domestic and international mail and parcels and specialize in dialogue marketing, nationwide press distribution services and all the electronic services associated with mail delivery.

The Express segment offers courier and express services to business customers and consumers in more than 220 countries and territories. Today, DHL generates almost 20% of its revenue in the Asia Pacific region. Just as FedEx has pioneered express distribution in the U.S., DHL’s CEO Ken Allen has claimed that “DHL pioneered Express services in Asia”.

The Global Forwarding, Freight segment handles the carriage of goods by rail, road, air, and sea. DHL is the world’s number one air freight operator, number two ocean freight operator, and one of the leading overland freight forwarders in Europe.

The Supply Chain segment is the global market leader in contract logistics, providing warehousing, managed transportation, and value-added services at every link in the supply chain for customers in a variety of industries. DHL also offers solutions for corporate information and communications management tailored precisely to the needs of customers.

REVENUES AND COMPETITION

Before diving into the analysis a few technical disclosures need mentioning to aid readers.

All year-to-date, or YTD, growth rates are based upon the most recent quarter’s data. The growth rate is compounded quarterly, CQGR, and annualized to reflect a current snapshot of the most recent 2-year growth trend. The baseline year of comparison is as follows:

- FedEx. 8/31/2011

- UPS, 6/30/2011, and

- DHL, 6/30/2011

This method is utilized in all subsequent sections comparing YTD growth rates, unless otherwise noted. Additionally, a year-over-year percentage change is included to accommodate for seasonality trends, unless otherwise noted.

All DHL revenue line items are based in Euro currency. As of the writing of this article, the Euro/Dollar conversion rate was €1.00 equals $1.3067. Please use the following link for any currency conversion interests or needs.

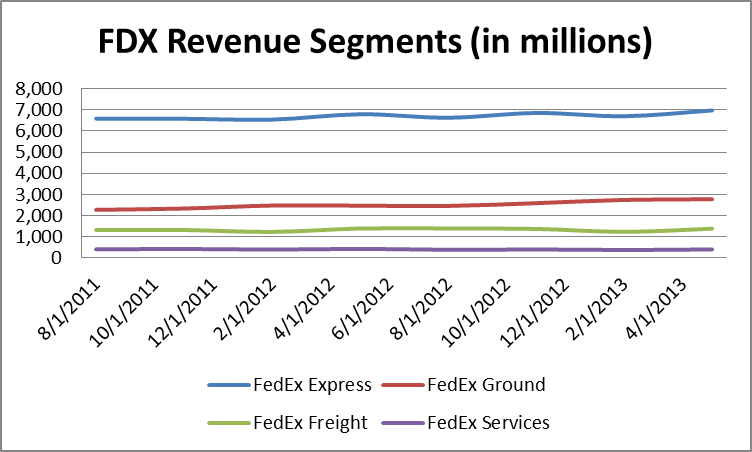

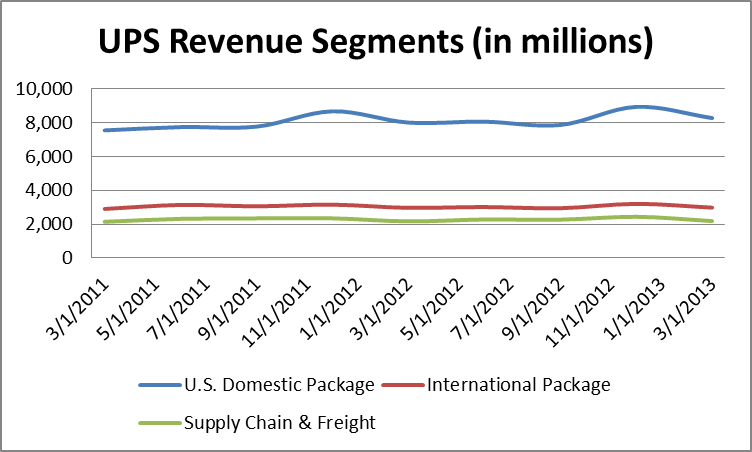

FedEx, UPS, and DHL provide mostly similar revenue line items in somewhat varying forms. The three charts below provide each company’s revenues by business segment.

(Click to enlarge)

(Click to enlarge)

(Click to enlarge)

At first glance, revenue growth has not been very exciting for these companies, considering their business segment revenues. However, these charts begin to illustrate characteristics regarding where these companies excel, for instance, FedEx generates a significant amount of revenue from its Express segment, UPS generates a significant amount of revenue from its U.S. Domestic Package segment, and DHL has a diversified range of revenue between €3-4 billion for all four segments.

Comprehensively, all three companies generate a substantial amount of revenue. The table below provides comparative growth rate trends based on total revenues. Trailing twelve-month revenues reflect each company’s most recent financial disclosure in 2013.

When considering total revenues, FedEx provides the most growth with the exception being the most recent year-over-year performance. It is important to note that while DHL clearly generates more revenue than all three companies, roughly one quarter of this total comes from the Mail segment which functions more like the U.S.’s USPS, within Germany. While both FedEx and UPS do provide services that are entrenched with the USPS, it is of interest to exclude the DHL Mail line item for comparative purposes. When considering DHL’s revenue growth rates without the Mail segment, it becomes clear that based on the company’s strong presence in Europe and Asia, there may be more competitive factors affecting FedEx and UPS growth.

The table below provides information regarding express-based package revenues. For FedEx this includes FedEx Express; domestic and international package line items, for UPS this includes U.S. Domestic Package; Next Day Air and Deferred line items and International Package; Domestic, Export, and Cargo line items, and for DHL this includes the Express line item.

It is not clear as to the proportion of DHL U.S. revenue, and based on the growth rates by FedEx and UPS combined with 2012 Latin America trade flows to Asia; it would not be a far fetch to assume that a majority of DHL’s growth may be occurring from Latin America. What is clear is that DHL is significantly outperforming its U.S. counterparts in the international geographies. FedEx appears to be a strong second ahead of UPS. This table suggests that UPS has been feeling pressure over the past couple years for its non-U.S. operations, and the pursuit to acquire TNT Express was a strategy to leap frog the competition. Improvements to the Cologne facility are in direct competition with DHL and TNT Express.

For ground-based revenues the table below provides pertinent information. For FedEx this includes FedEx Ground, and for UPS this includes the U.S. Domestic Package Ground line item. DHL’s closest product that resembles this area is its Mail Parcel Germany line item. This line item seems to function as a hybrid USPS-like mail delivery and ground-based parcel service.

For those not entirely familiar with UPS, this is the company’s bread and butter segment. With a history dating back to 1907, the company has developed into the U.S.’s dominant ground parcel delivery service. To FedEx’s credit, this segment represents its second fastest growth driver. In just over a third of UPS’s company history, FedEx has grown to nearly 50% of UPS’s ground revenues. DHL is experiencing robust parcel delivery growth within Germany.

For freight forwarding and supply chain revenues the table below provides pertinent information. For FedEx this includes the FedEx Express Other line item, for UPS this includes the Supply Chain and Freight; Forwarding and Logistics line item, and for DHL this includes Global Forwarding, Freight and Supply Chain; Global Forwarding and Supply Chain line items.

FedEx has experienced extremely significant growth in the company’s FedEx Trade Networks and FedEx Supply Chain Systems areas; grouped collectively in the FedEx Express “Other” revenue line item. Apparently, UPS has struggled recently. Similar to UPS’s Ground segment, forwarding and supply chain operations are DHL’s strong point. The company has plenty of examples of supply chain ventures in China. As DHL is such a dominant force in this area it is beneficial to expand upon the company’s developments.

As mentioned, DHL already generates almost 20% of its global revenue in the Asia Pacific region. By 2017, the company plans to increase revenue in the region to a third of its total. In the last several years DHL has invested more than 2.5 billion U.S. dollars to develop products and services in Asia. In addition, the company plans to invest in further aircraft in order to serve the high-demand trade lanes between Shanghai, northern Asia, Europe, and the U.S.

Source: DHL Annual Report 2012

For freight-related revenues the table below provides pertinent information. For FedEx this includes the FedEx Freight line item, for UPS this includes the Supply Chain and Freight; Freight line item, and for DHL this includes the Global Forwarding, Freight; Freight line item.

Both FedEx and DHL have a lead on UPS with respect to freight revenues. This market segment is highly fragmented and there are many other competitors in North America representing LTL and full truckload services including companies like Con-Way Inc. (CNW) and YRC Worldwide Inc. (YRCW), among others.

Revenues and Competition Summary

Based on the revenue analysis it is clear that FedEx Express, UPS Ground, and DHL’s Freight Forwarding and Supply Chain line items are the most significant areas for each respective business. When comparing FedEx to UPS, the only area where UPS is slightly outpacing FedEx is in freight-related revenues. FedEx is outperforming UPS significantly in all other major revenue areas, and will continue to chip away at UPS’s total revenue lead. DHL seems to be competing much better against FedEx from a growth perspective, granted in some respects DHL is at the lowest end of the group. DHL’s core success for the foreseeable future will rely upon its forwarding and supply chain operations; the company is also seeing strength in its Express segment and within Germany.

KEY GROWTH DRIVERS

Key growth drivers for express and ground-based revenues will include average daily package volumes, or ADVs, and revenue/package yields. Key growth drivers for freight revenues will include freight LTL shipments, weight/LTL shipment, and LTL yield (revenue/hundredweight). It should also be noted that in this section, all YTD data is not annualized and therefore, there is no need for YOY comparisons.

For express-based package ADV and yield, the table below provides trailing twelve-month, or TTM, information. For FedEx this includes FedEx Express; domestic and international package ADV and revenue/package yield, for UPS this includes U.S. Domestic Package; Next Day Air and Deferred package ADV and revenue/package yield, and International Package; Domestic, Export, and Cargo package ADV and revenue/package yield, and for DHL this includes the Express package ADV.

What is clear between FedEx and UPS is that U.S. revenue/package yields are fairly close and FedEx’s slightly higher volume and yield is the reason why the company has generated more U.S. express-based package revenue. It should be noted that FedEx disaggregates its freight-related express operations into freight revenue/pound yield, while UPS does not. It would also appear that UPS has taken some U.S. package ADV market share of late.

Non-U.S. express revenue/package yields tell a completely different story. FedEx is able to generate a 52% higher comprehensive yield than UPS (this is declining significantly of late), which allows for them to generate 40% less volume and come within 17% of UPS’s Non-U.S. express-based package revenues.

FedEx is also growing extremely fast with respect to Non-U.S. package volumes, driven predominantly by international domestic services at 8.5%. This is a direct result from acquisitions in 2012 including the Mexican domestic express package delivery company Servicios Nacionales Mupa, S.A. de C.V. (Multipack); the Polish domestic express package delivery company Opek Sp. z o.o.; the French express transportation company TATAEX; and the Brazilian transportation and logistics company Rapidao Cometa Logistica e Transportres S.A.

FedEx managed growth near 1.0% for its international export services. These two services provide the company’s lowest and highest revenue/package yields respectively.

While total global package volume growth for Express services was strong for DHL, this information is not broken down geographically and revenue/package yield was not available.

For ground-based package ADV and yield, the table below provides pertinent information. For FedEx this includes the FedEx Ground package ADV and revenue/package yield line items, for UPS this includes the U.S. Domestic Package; Ground package ADV and revenue/package yield line items, and for DHL this includes the Mail; Parcel Germany package ADV.

When comparing UPS to FedEx package ADV, UPS produces almost double the package volume. FedEx returns the doubling effect outpacing UPS based on the growth rate, however, when we consider where this growth is coming from, it is clear that FedEx SmartPost is leading the way growing at a CQGR near 5.5% and while the FedEx Ground segment is growing near 1.8%.

This becomes clearer when considering yield information. Although it appears that FedEx is able to command a 10% premium for its revenue/package yield, 33% of FedEx’s package ADV is generated from FedEx SmartPost which produces a revenue/package yield of $1.77. If we were to average both of these segments, FedEx would have a yield of $6.60.

So while FedEx is making significant progress with ground volumes, their revenues may not necessarily reflect this growth based on the lower yields generated from SmartPost.

DHL similarly to the express-based segment displays significant volume growth in Germany, with no information related to yields.

For freight LTL shipments, weight/LTL shipment, and LTL yield (revenue/hundredweight), the table below provides pertinent information. For FedEx this includes the FedEx Freight line item, for UPS this includes Supply Chain and Freight; Freight line item, and for DHL there was not sufficient comparative information to be included.

Both FedEx and UPS compare closely when considering freight drivers. The primary variable distinguishing between the two is the fact that FedEx provides more average daily LTL shipments, which strongly correlates to freight revenues.

Key Growth Drivers Summary

Unfortunately, this section does not provide a complete comprehensive analysis for DHL. The available trends do however speak to the fact that DHL is growing well within Germany, and other international geographies.

The highlight from this information when comparing FedEx and UPS seems to be that FedEx’s growth drivers continue to exceed that of UPS. When assessing the value of FedEx’s growth, we can see that some of their lower revenue/package yield services including international domestic (via acquisitions) and FedEx SmartPost are leading this trend. This speaks to the competitive strength of UPS’s domestic Ground services and domestic express-based package services, as FedEx is taking alternative strategies to grow its package and parcel volumes.

On the acquisition front, FedEx has recently acquired a South African company, Supaswift and its subsidiaries. This deal should have similar implications, namely reducing international yields and increasing international volumes, and marginally increasing international express revenues.

It would also appear that FedEx is better positioned with respect to freight services for express-related packages and LTL freight shipments. FedEx’s focus of taking volume market share from UPS within these focus areas may end up paying off in the long-term, but remains to be seen.

For other categories without growth drivers including Freight Forwarding and Supply Chain, investors should assume the above high-level developments for world GDP and oil prices. FedEx’s supply chain services are the fastest growing segment within the company, while UPS is losing market share, and DHL’s dominant presence is only getting stronger.

FUNDAMENTAL PEER REVIEW

To be honest this is my favorite part of the analysis. With the above information in the back of our minds, we now will be able to consider stock price growth over time, debt/equity, free cash flow/share growth, earnings/share growth, among many other metrics. Rather than divulge them all in written form, let’s get right to it with the table below and accompanying charts. All data is as of the market close, June 25, 2013, and is based on TTM and diluted shares outstanding where appropriate.

This table presents us with what I like to call a conundrum. FedEx is the fastest growing company between the three, yet has the lowest enterprise value by a wide margin compared to UPS, and more slightly versus DHL. Based on FedEx’s broad strength leading in five of the eight other categories, it does not necessarily make sense for the company to trade at such a depressed EV/sales ratio.

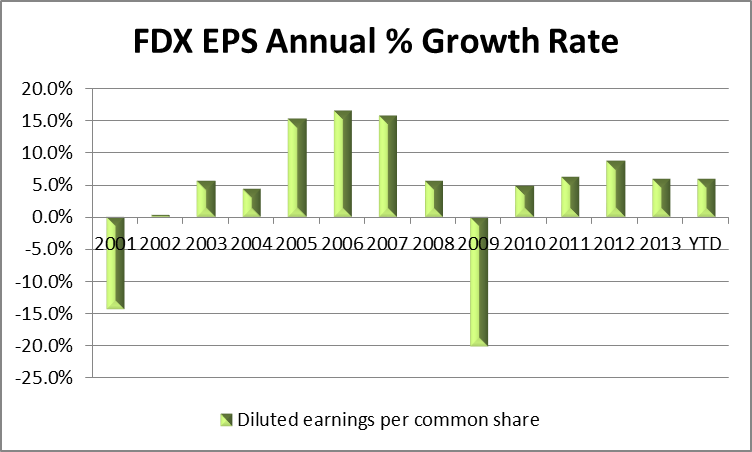

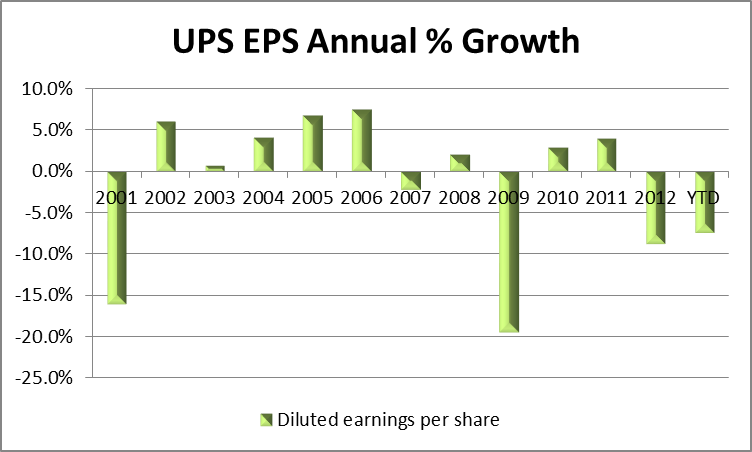

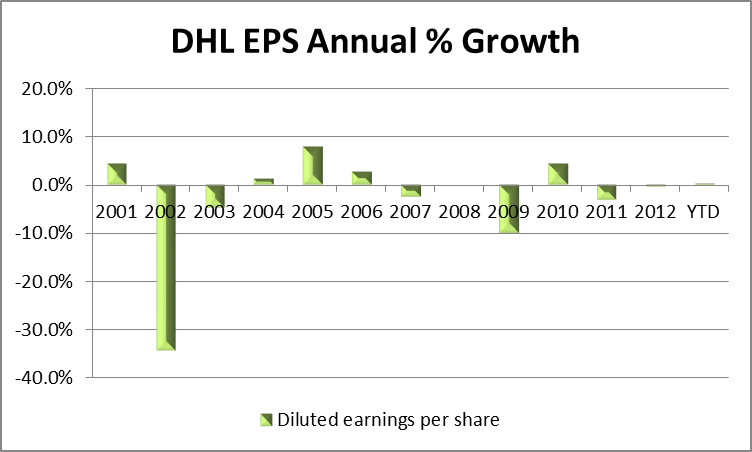

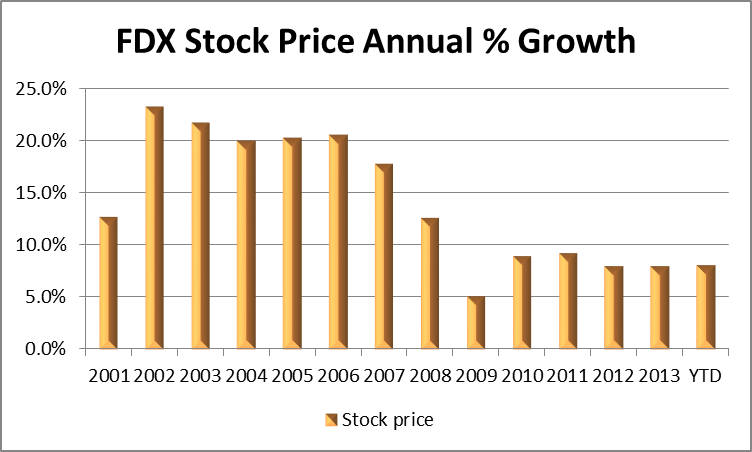

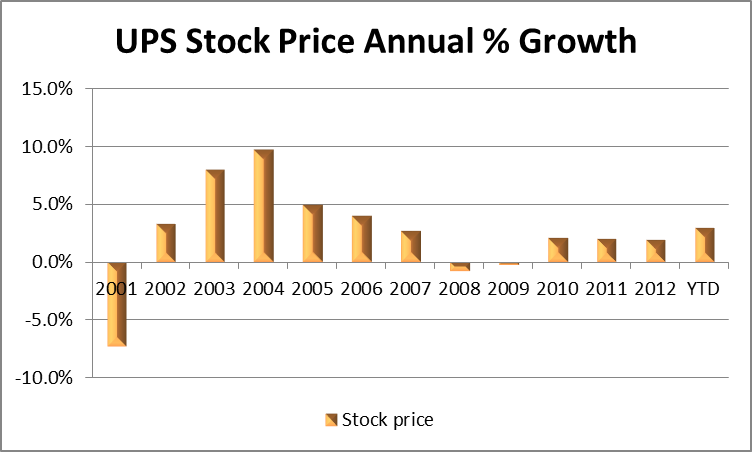

The charts below will compare key trends related to earnings per share growth, stock price growth, free cash flow per share growth, and dividend growth, to paint a picture of these core growth drivers.

(Click to enlarge)

(Click to enlarge)

(Click to enlarge)

When comparing diluted earnings per share growth, the effects of the two recessions are clearly prevalent in 2001/2002 and 2009 performance. FedEx provides the most consistent growth hovering around the 7% level the previous four years. UPS’s recent earnings decline is somewhat deceiving as it was a result of one-time pension costs. We can see that the 2013 Q1 result has already improved the YTD marginally for UPS. DHL has struggled throughout the previous ten-plus years to produce positive earnings.

(Click to enlarge)

(Click to enlarge)

(Click to enlarge)

For investors who have owned FedEx stock over the past decade, returns have definitely been kind. Post-recession returns have fluctuated between 8-9% per year. UPS’s stock price has grown at a slow pace during the decade, and DHL, while negative throughout the entire decade has provided some great buying opportunities near their lows.

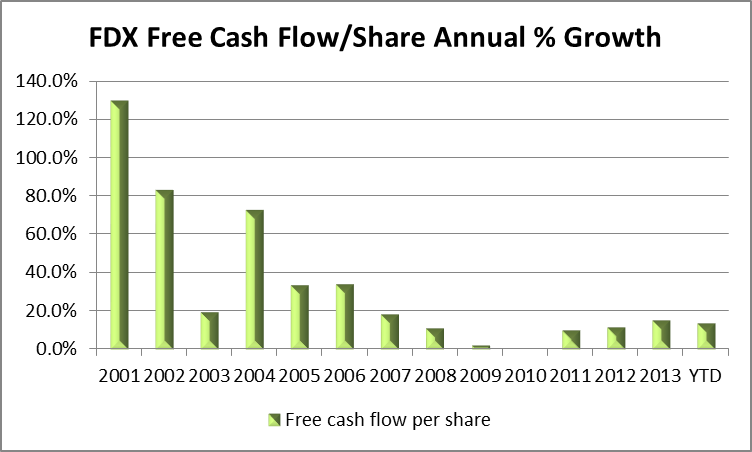

(Click to enlarge)

(Click to enlarge)

(Click to enlarge)

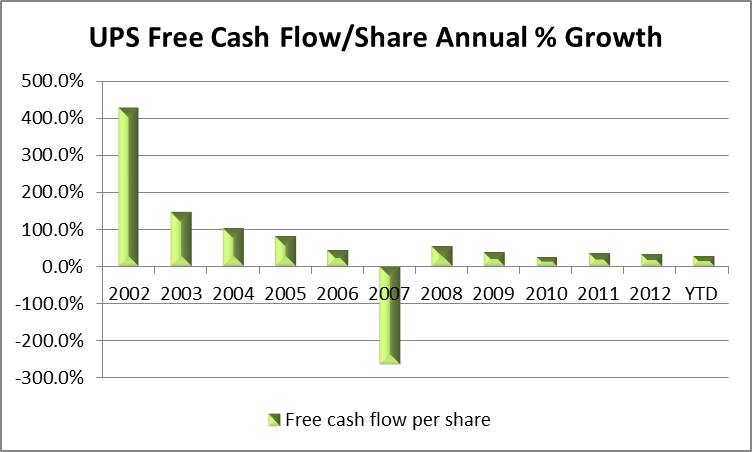

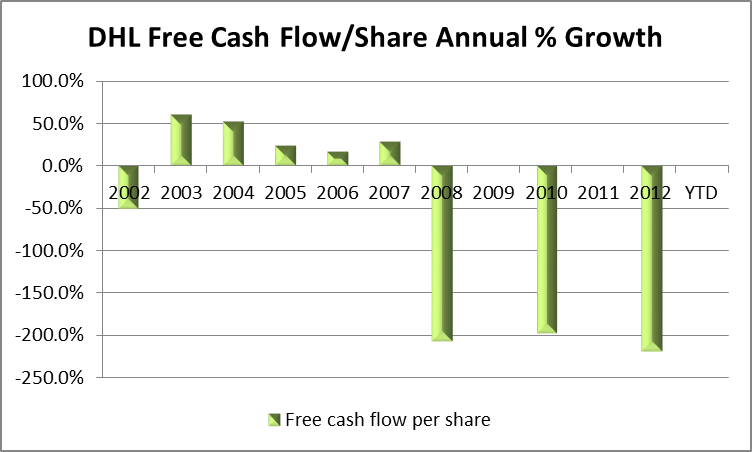

Personally, free cash flow per share carries the most weight for most of my investment considerations as this metric solidifies a company’s operating strength to fund capital expenditures, dividends, and debt obligations, among other financial items. Both FedEx and UPS have generated significant free cash flow per share growth during the previous decade at an annual rate of 14% and 28% respectively. DHL has struggled with negative free cash flow the past five years.

The strength of this metric is reflected in capital expenditures as FedEx has averaged over $3.2 billion the past five years, UPS has averaged $2 billion, and DHL has average €1.5 billion. Despite UPS and DHL’s close capital budgets, UPS has also averaged an additional $1.8 billion per year in stock repurchases.

(Click to enlarge)

(Click to enlarge)

(Click to enlarge)

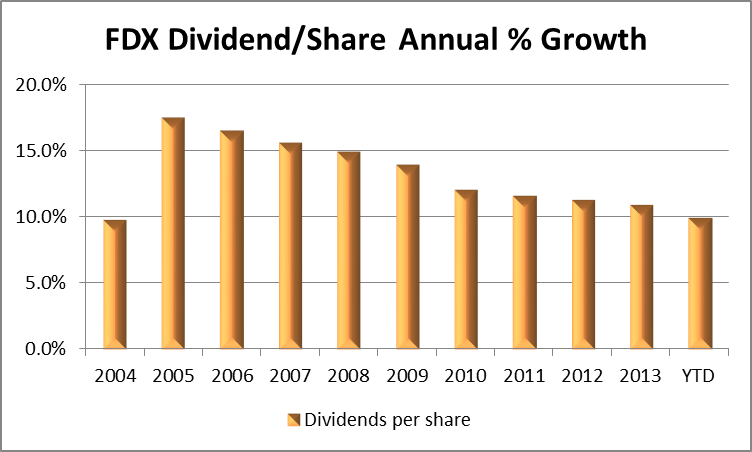

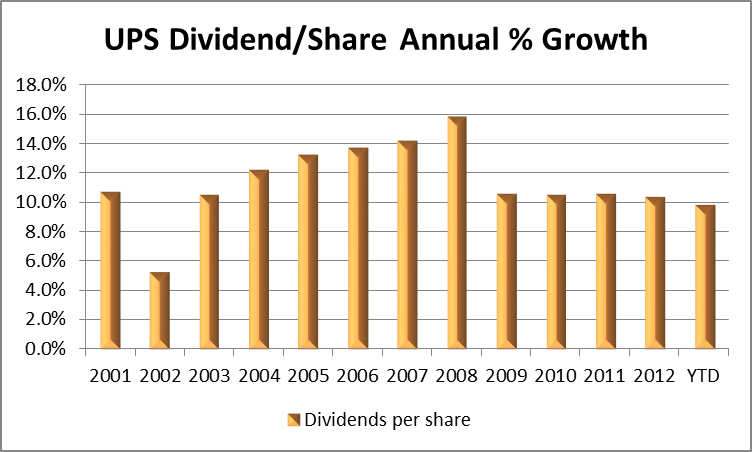

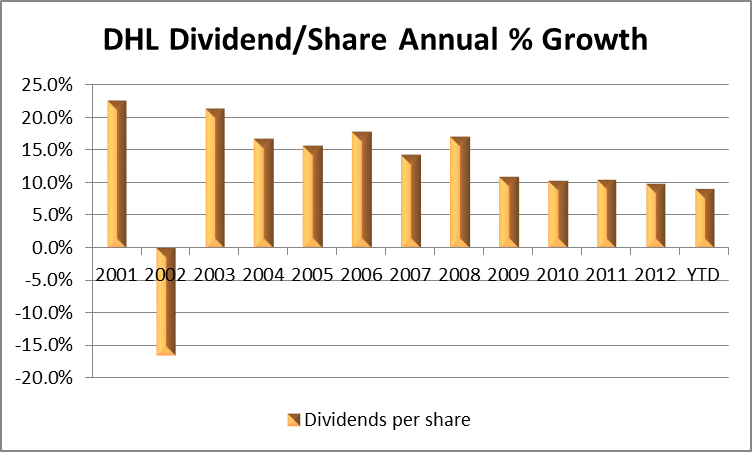

All three companies have averaged a 10% dividend growth rate per year. DHL’s dividend has typically yielded a slightly higher amount than UPS, while FedEx, despite solid dividend growth, would take far too long to get to any level close to UPS or DHL, unless they significantly raised their dividend payout.

Fundamental Peer Review Summary

For me the bottom line for FedEx is that the company continues to display leading revenue growth characteristics, while having a significantly depressed enterprise value. The company is financially sound based on its leverage and cash flow generation. FedEx’s investments in more fuel-efficient airplanes including greater carrying capacity should improve operating margins and ultimately lead to increased cash flows.

The closer FedEx gets to UPS based on revenue and cash flow generation, the stronger the argument for a more consistent valuation, which bodes well for FedEx shareholders.

CONCLUSION

All three of these companies possess significant strengths. FedEx has grown rapidly over the past 40 years pivoting off of its express services. UPS is a dominant force in the U.S. via its Ground segment, while DHL rules the global freight forwarding and supply chain arena.

FedEx iterated guidance of earnings per share growth between 7-13% based upon modest GDP growth of 2% in the U.S. during 2013 and 2.5% during 2014. With all of the capital investments and asset disposals, the company is targeting annual profitability improvement of $1.6 billion by 2016 at its Express segment.

The company also expects earnings and revenue growth for its Express segment this upcoming year and revenue growth for all Ground services based on e-commerce trends, market share gains, and yield growth. Freight is expected to grow modestly.

Headwinds include continued pressure on international yields and freight volumes. Please refer to the earnings transcript for more details.

On a more speculative note there may be opportunities for FedEx to continue to partner with and/or consolidate aspects of the USPS, which is in a risky financial position. The following link provides the agency’s most recent 10-K filing. The agency’s current liability challenges involve $11.2 billion in retiree health benefits and $9.5 billion in current debt. This does not even include the agency’s regular compensation and benefits or payables and accrued expenses which total $3.7 billion. The company only has $3.4 billion in current assets. Between 2011 and 2012, the USPS net deficit has grown from ($18.9) billion to ($34.8) billion. Many of the USPS volume trends are continuing to decline including First-Class Mail, Standard Mail, Periodicals, and Other services.

While it does not make sense for FedEx, UPS, or DHL to attempt to acquire the USPS business collectively, it would make sense for the USPS’ services to eventually become privatized. This may occur on a more segmented basis. DHL’s counterpart Deutsche Post is a proven record that a national mail operation can fit within a well-established global package, freight, and supply chain company.

Overall, DHL’s logistics operation is the most intriguing part of the company’s future, yet as it is a German-based company most U.S. investors will probably not necessarily be interested in purchasing shares. UPS provides a strong incentive for investors via its dividend payout and growth, as well as its leadership in free cash flow growth. FedEx, however, seems to be a stronger candidate as the leader amongst these three peers based upon the company’s key growth drivers, revenue growth trends, and comprehensive fundamental strength.

Disclosure: I am long FDX. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

FedEx Versus UPS And DHL, A Comparative Analysis Of Global Logistics Giants

Không có nhận xét nào:

Đăng nhận xét